14 minute read

Apr 2025

CONTRIBUTORS

Ilya Epikhin

is a Senior Principal and Global Head of Arthur D. Little’s Natural Resources Competence Center and Energy, Utilities & Resources practice and based in the Dubai office.

Amer Hage Chahine

is a Partner in Arthur D. Little’s Energy, Utilities & Resources practice and based in the Dubai office.

Carlo Stella

is a Managing Partner and Global Practice Leader of Arthur D. Little’s Sustainability practice and based in the Dubai office.

Trung Ghi

Partner, Energy, Utilities & Resources

In 2024, the intensity rose in a growing geopolitical battle across the world’s great oceans. Seabed mining — extracting critical minerals essential for batteries, electric vehicles (EVs), and other green technologies — is a US $20 trillion opportunity. Looking ahead, land mining alone is unlikely to be sufficient to meet the forecast demand. Meanwhile, seabed deposits are huge, and the technology is becoming increasingly feasible. It will likely revolutionize the minerals mining industry.

Some countries, such as China, Japan, Belgium, Canada, and Norway, are already testing deep-sea mining technologies within their own national jurisdictions. China, especially, is looking to take a global leadership position and already has more exploration licenses for international waters than any other country. Given that China already controls ~95% of the world’s supply of rare earth metals and produces about three-quarters of all lithium-ion batteries, the US and other Western countries see this possible future supply dominance as a major threat.

Seabed mining is also controversial because of its potential environmental impacts; it is not yet permitted in international waters, pending new regulation now expected in 2025. It is by no means certain whether this will lead, as it should, to a future of ethical, sustainable, and profitable extraction or whether cooperation will break down, leading to the possibility of unregulated and potentially damaging exploitation. In this article, we look at the key issues affecting the future of seabed mining and explore the priorities for key stakeholders, including governments, metals/mining companies, and oil/gas companies, to help ensure a positive future for the industry.

Why Seabed Mining Matters

Seabed mining involves the extraction of minerals, such as manganese, cobalt, nickel, copper, zinc, and, to a lesser extent, gold, silver, and rare earth metals, which exist in deposits on the surface of the seabed.

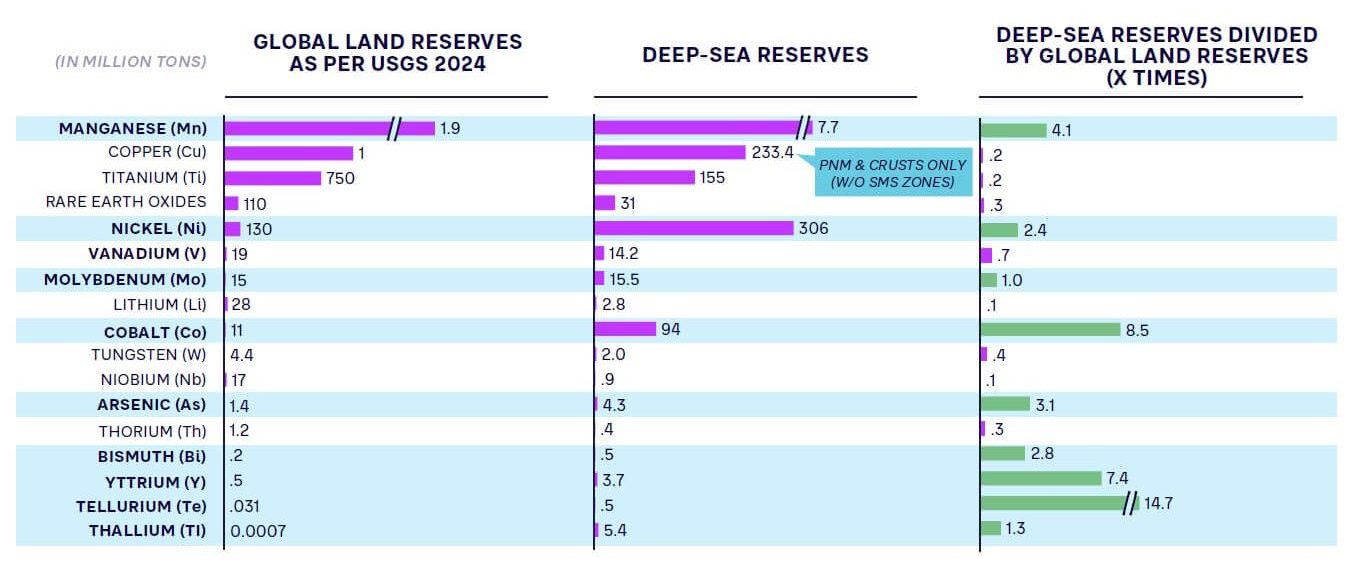

Deep-sea reserves for manganese, nickel, cobalt, and several rare earth minerals are many times larger than land reserves (see Figure 1).

Figure 1. Global deep-sea versus land reserves

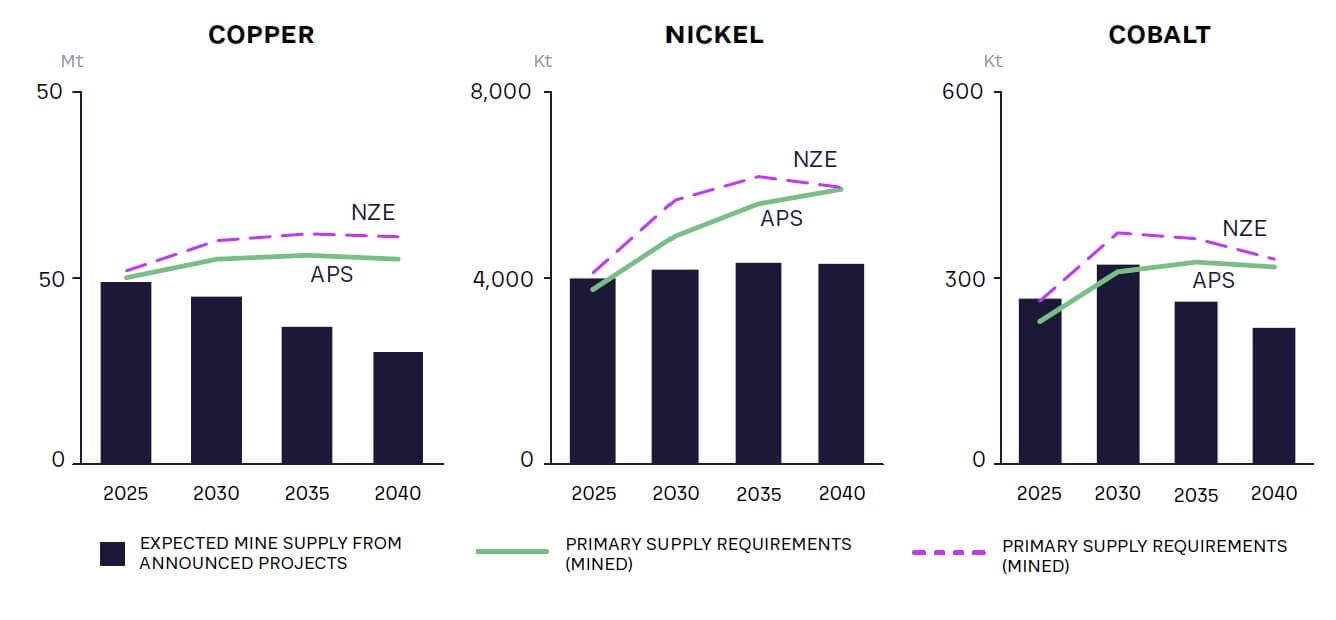

Looking at future demand, if we assume either the Announced Pledges or Net Zero Emissions scenario according to the International Energy Agency’s modelling, over 20 years, there will be a major shortfall in supply from land mining alone, at least for copper, nickel, and cobalt (see Figure 2).

CONTRIBUTORS

Ilya Epikhin

is a Senior Principal and Global Head of Arthur D. Little’s Natural Resources Competence Center and Energy, Utilities & Resources practice and based in the Dubai office.

Amer Hage Chahine

is a Partner in Arthur D. Little’s Energy, Utilities & Resources practice and based in the Dubai office.

Carlo Stella

is a Managing Partner and Global Practice Leader of Arthur D. Little’s Sustainability practice and based in the Dubai office.

Trung Ghi

Partner, Energy, Utilities & Resources

Figure 2. Projected demand for copper, nickel, and cobalt versus land mining supply

The manganese shortfall is even more extreme, with global supply needing to increase by a factor of 10 to meet the forecast 2030 demand. Given that China has a near monopoly on land mining of these critical minerals, many countries see supply diversification through seabed mining as strategically vital.

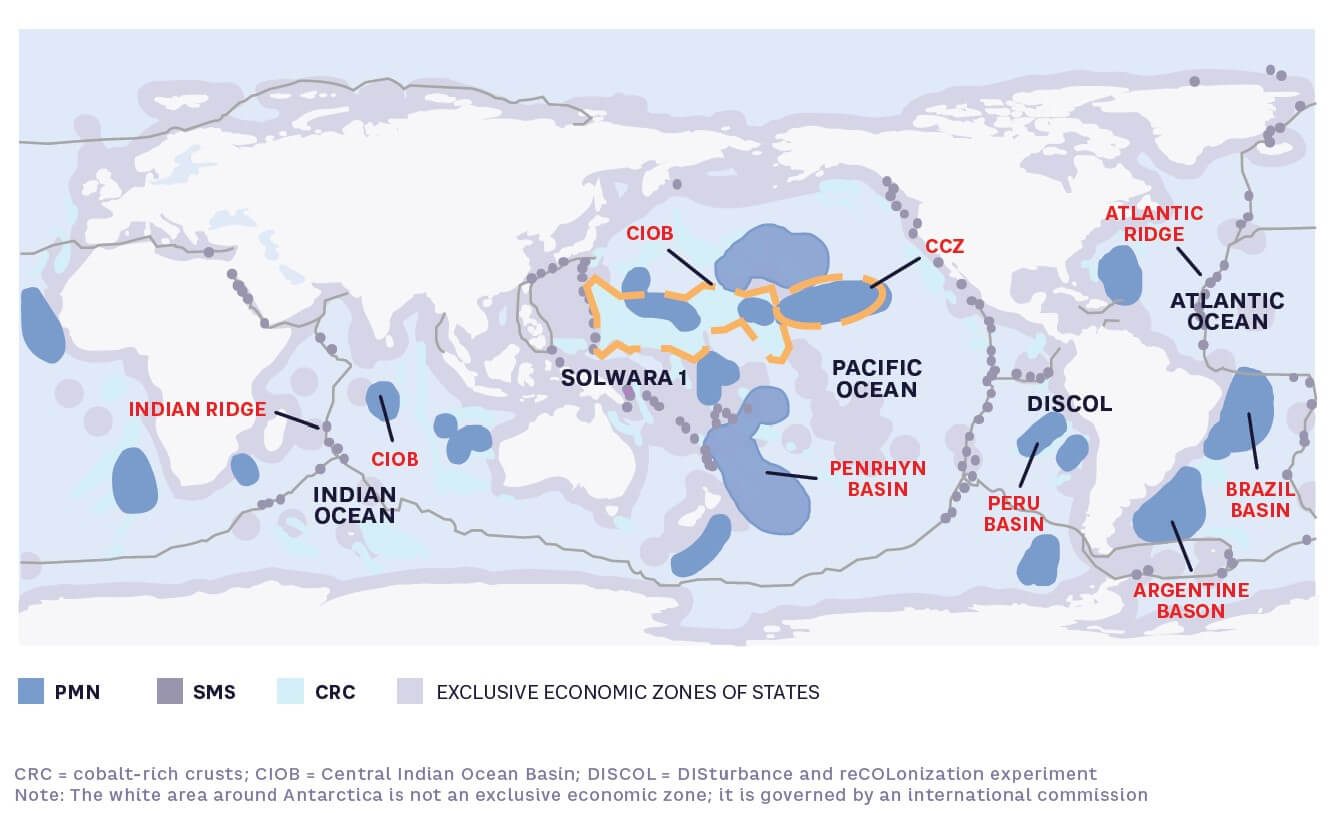

One of the most intriguing aspects of seabed mining is that the largest deposits are in international waters, especially the Pacific Ocean, as well as the Atlantic and Indian Oceans, posing particular geopolitical and regulatory challenges (see Figure 3).

Figure 3. Known global mineral deposits relevant for seabed mining

The most abundant and valuable deposits are polymetallic manganese nodules (PMN), which contain nickel, copper, cobalt, and manganese. These nodules, which vary in size from a few millimeters to the size of a small potato, occur on the surface of the seabed, mainly in the Pacific Ocean at water depths below 3,500 meters. The typical PMN nodule composition of manganese, nickel, copper, and cobalt is especially well suited for manufacturing batteries for EVs and other devices.

A second deposit type is cobalt and manganese-rich crusts (CRCs), which contain manganese, copper, nickel, and other trace minerals. These are deposited on bare rock surfaces up to 10-20 cm in thickness, usually in shallower waters. The largest known CRC deposit is the Prime Crust Zone (PCZ) in the northwest Pacific.

A third type of deposit is known as seafloor massive sulfides (SMS), which comprise mainly copper, zinc, silver, and gold and are located at hydrothermal vents along mid-ocean ridges 1,500-3,000 meters down.

Retrieving these deposits from deep waters is technically challenging. The pressures can be 500x atmospheric pressure, and temperatures can range from 2 degrees Celsius at the seabed to 400 degrees Celsius at hydrothermal vents.

Unmanned underwater vehicles, either autonomous or remote- controlled, can collect minerals efficiently while navigating obstacles. The most effective method to get the material to the surface is to use pipeline lifting systems consisting of riser pipes extending from the seafloor to a surface vessel, through which powerful pumps suck up the slurry. Environmental impact is mitigated through various means, such as sediment containment systems to minimize the dispersion of disturbed sediments and precise, targeted extraction techniques to avoid unnecessary damage to surrounding habitats.

The retrieval costs are currently high: collection vehicles cost $10–$20 million each, support vessels cost $400–$600 million, and riser air–lift systems cost $200–$300 million. However, recently proposed alternative approaches, in which multiple small autonomous underground vehicles (AUVs) hover just above the seabed to collect nodules selectively, could have lower CAPEX costs and be more environmentally friendly.

A greenfield processing plant that can handle seabed materials could cost $3–$4 billion. Economic viability at scale has not yet been demonstrated. However, the industry is becoming increasingly commercially viable with technological advances and a growing partnership ecosystem.

“The retrieval costs are currently high: collection vehicles cost $10 – $20 million each, support vessels cost $400 – $600 million, and riser air-lift systems cost $200 – $300 million”

The current state of play

Exploration and exploitation are regulated by the International Seabed Authority (ISA), established in 1995 under the United Nations Convention on the Law of the Sea (UNCLOS). Today, it has 168 member states, with the notable exception of the US, which refused to join. After many delays, in 2025, the ISA is expected to finally issue regulations that will commence exploitation.

Governments worldwide are investing in seabed mining. China, in particular, holds five of the 30 exploration licenses issued by the ISA and is the leading player globally. Japan is also investing heavily in seabed mining technology and exploration. Other countries, such as India, are growing their presence. Russia already holds two licenses.

After almost five years of discussions, Norway became the first country to approve mineral exploration and exploitation on its own continental shelf in 2021. Exploratory activities are also underway in other continental shelves, including New Zealand, South Africa, Namibia, Papua New Guinea, and the Solomon Islands.

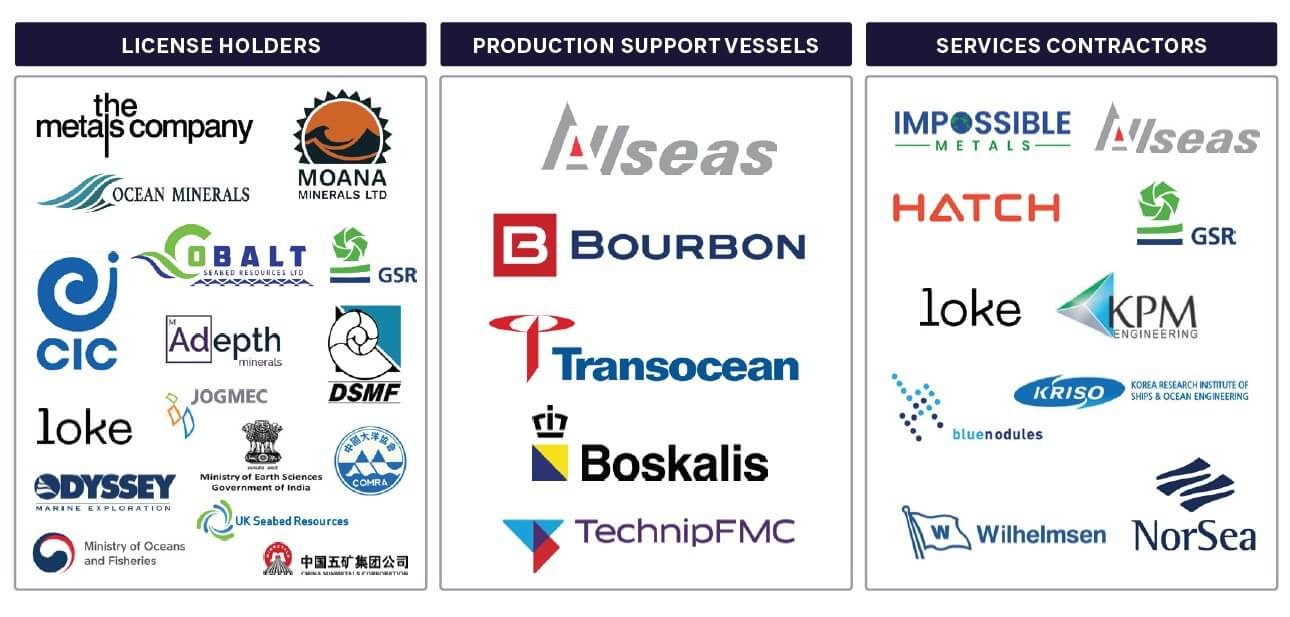

An ecosystem of commercial players is already well-established, comprising license holders, production support vessels, and services contractors (see Figure 4).

Figure 4. Companies currently operating in the seabed mining ecosystem

Key Challenges Going Forward

The industry faces tough challenges in three areas: environmental, technological/economic, and geopolitical/regulatory.

Environmental Impact

There is no perfect method of extraction. The environmental impacts of seabed mining include disturbance of habitats and fauna, water plume generation, and light/noise/vibration from surface operations. However, the recently proposed multiple AUV selective extraction approach would minimize seabed disturbance. In any case, it is important to balance these impacts against the benefits. Compared to terrestrial mining, seabed mining can have a substantially lower environmental footprint with fewer disturbances to ecosystems and landscapes. Nodule deposits are generally located in ecosystems with less life and lower levels of biodiversity than virtually all other ecosystems, whether oceanic or terrestrial. Life is virtually nonexistent at extreme depths of up to 6,000 m.

Moreover, comparisons of seabed mining to existing land mining operations have shown dramatically lower lifecycle carbon emissions. According to The Metals Company, a comparison for nickel shows 6.2 kg CO2 per kg nickel for seabed mining versus typically between 20 and 100 for land-mining operations. While it could be argued that comparing seabed mining with another environmentally damaging activity is not in itself a justification, if we accept that the minerals have to be mined somehow — and demand will increase rapidly if we are to implement the green transition successfully — then it has a net beneficial effect. Indeed, without seabed mining, the green transition will be difficult to achieve.

However, the seabed is a pristine environment, and understanding the full ecological implications of seabed mining is not straightforward. For this reason, apprehension among scientists, environmentalists, and governments persists.

Technological and Economic Feasibility

Technological challenges exist across all parts of the extraction process, including mineral collection systems, mining vehicles, subsea lifting systems, and surface support systems. Subsea lifting systems are especially important, accounting for more than 50% of the energy consumption of the whole mining process.

“Recent innovations are making seabed mining increasingly feasible. Many innovations have been made in mining vehicles to improve their efficiency, precision, and environmental impact”

Recent innovations are making seabed mining increasingly feasible. Many innovations have been made in mining vehicles to improve their efficiency, precision, and environmental impact. For example, vehicles that combine autonomous navigation with operator control for precise tasks use sensors and AI to identify resource-rich areas and adapt operations in real time to collect material. Innovations such as corrosion-resistant alloys, high-strength composites, and real-time monitoring systems enhance the reliability and efficiency of collection methods and lifting systems.

While commercial viability is improving, there is still some way to go. Financing will only become available when miners demonstrate their ability to deliver at an industrial scale (i.e., over 500,000 tons annually). If operations cannot be shown to be sufficiently profitable, then seabed mining may hit a “trough of disillusionment” before it finally becomes established.

Geopolitical and Regulatory Challenges

Access to critical mineral resources for future economic and environmental sustainability is an important strategic issue for any state. The ISA has the daunting task of overseeing seabed mining activities in international waters, including protecting the marine environment, promoting marine scientific research, allowing for equitable sharing of financial and other economic benefits, and ensuring participation and capacity building by the smaller, developing states. It achieves the latter through its licensing policy, which provides preferential access to developing states for reserved exploration areas. Revenue sharing and royalty agreements between mining companies and host countries are critical components of subsea mining models, ensuring mutual benefits from resource extraction.

One of the challenges facing global regulation is the noninvolvement of the US in the ISA — it only participates as an observer. It has been suggested that the US did not wish to ratify the Law of the Sea because the “one vote per country” modus operandi of the ISA for decision-making was not considered beneficial — the US would have no more power than any of the other 160+ ISA members. However, the US has not explained its position, so this can only be conjecture. The US is short of critical minerals and severely import-dependent. At the time of writing, the Republican Party had just won the US presidential election, so we can expect a more aggressive policy going forward, seeking to establish US metals sovereignty, streamlining permitting, and possibly even going as far as becoming a net exporter, similar to the shale oil revolution of 2010–2020.

In the meantime, China has already established a dominant position. From a corporate perspective, one of the leading mining companies is Canadian-based TMC, which is applying for a license to start mining in 2025, further strengthening its position in the global resource sector. Other significant players, such as Impossible Metals, are emerging, offering more environmentally friendly AUV technologies for selective seabed mining.

If the ISA misses the deadline for issuing seabed exploitation law next year, a near future of unregulated exploitation is possible. In this situation, companies such as TMC could start production anyway, likely to be followed by others. There is currently no restriction in international law to prevent this. The US could become involved if the ISA authority starts to break down. An unregulated scenario brings obvious risks of environmental damage and even conflict.

“One of the challenges facing global regulation is the noninvolvement of the US in the ISA — it only participates as an observer”

Insights for the Executive

With land-based mining challenged by declining ore grades, stricter environmental regulations, and rising costs, seabed mining is potentially a $20 trillion opportunity, providing a chance for countries to diversify their portfolios and access higher-grade deposits of critical materials. It helps bolster countries’ global presence and geopolitical power. Larger countries also have national economic benefits through the development of new cutting-edge technologies in material lifting, transportation, and processing, bringing new sources of value, skills, and positive cashflows. However, the environmental, technical, economic, and geopolitical challenges must be carefully addressed.

No single company can currently manage the entire seabed mining process, from extraction to processing. Strategic partnerships between companies, including mining companies, technology providers, and oil and gas companies, will be crucial for overcoming technical challenges, sharing expertise, and ensuring sustainable practices. It is in everyone’s interests to avoid a collapse of collaboration and a future of unregulated exploitation. To ensure a positive future for seabed mining, the following priorities are therefore important for the key stakeholders concerned.

Governments

Governments must ensure they are not left behind, given that mining activity will likely begin as early as 2025. Countries not already holding a license need to quickly enter the space and apply, especially as remaining concessions are decreasing rapidly. In practice, this means:

- Engaging proactively with the ISA

- Selecting the right corporate licensing partner, a mining company that the government will sponsor

- Deciding national expertise needs and the required degree of outsourcing

- Assessing legal risks and consequences for different options and deciding which to pursue

- Setting up local national seabed mining regulations quickly to build on in developing their continental shelf operations (if this is applicable and they have access to the sea)

The major geopolitical battle is expected to be around fears of Chinese dominance, with the US entering the market aggressively in the near future.

Governments also need to ensure that the environmental concerns of academics, nongovernmental organizations, and the general public are recognized and, as far as possible, addressed through rational, scientific, evidence-based arguments controlled by robust regulation. The relatively less damaging environmental impact of seabed mining versus (otherwise unavoidable) land-based mining should be part of the discourse.

Metals and Mining Companies

Technology providers need to quickly develop the robotics, remote sensing, and subsea engineering essential for the efficient and sustainable extraction of seabed minerals. They should focus especially on improving business model viability, scaling up operations to industrial levels, and further enhancing environmental performance.

No mining company today can run the full end-to-end process involving collection, lifting, storage, offshore transshipment, transportation, delivery, processing, and conversion to the final product alone. This means establishing the right strategic partnerships — for example, between mining and processing companies — is also key.

Oil, Gas, and Shipbuilding Companies

The deepwater exploration, drilling, and infrastructure skills of oil and gas companies with offshore operations directly apply to seabed mining. Companies such as Shell and Total can leverage their offshore technology and expertise to explore seabed mining opportunities. Creating subsidiaries and joint ventures with those directly involved in seabed mining is a logical way forward. There will also be new opportunities for shipbuilders to refurbish existing oil and gas vessels and create new vessels suitable for seabed mining.

The Revolution is Coming

Despite the environmental risks, the economic and geopolitical forces driving seabed mining are strong. Therefore, a revolution in minerals mining is almost certainly coming. However, whether the revolution is peaceful or bloody (figuratively, at least) is still uncertain.

On the plus side, the ISA offers a well-established international framework for cooperation and regulation. Environmental risks are prominent on its agenda, and technology is rapidly improving. On the minus side, ultimately, the framework depends on voluntary compliance by the parties involved, and the absence of the US from the ISA creates uncertainty. What’s more, there is no effective means for enforcement of regulations. Monitoring multiple seabed mining operations in remote oceanic deep-sea locations will be extremely difficult. Each state must find its balance between risk and reward in a battle that will likely become increasingly intense. In today’s fractious geopolitical climate, businesses have an especially important role in ensuring responsible seabed mining in a spirit of trust and collaboration.