13 minute read

Jan 2026

Energy Crunch

CONTRIBUTORS

Luis del Barrio Castro

Partner, Energy, Utilities & Resources

Michael Kruse

Managing Partner, Energy, Utilities & Resources

Sean McDevitt

Partner, Telecommunication, IT, Media & Electronics

Lars Riegel

Partner, Telecommunication, IT, Media & Electronics

Michael Liebreich

Energy Analyst & Founder, Bloomberg New Energy Finance

Dr. Albert Meige

Global Director, Blue Shift and Lead Author, AI's Hidden Dependencies

Since the launch of ChatGPT, AI’s growth has appeared inevitable and unstoppable, with the world’s biggest companies throwing billions of dollars into creating the world’s newest infrastructure. Because it lives mainly in the cloud and on our screens, AI appears to be a benign, almost weightless extension of the Internet, removed from earthly concerns like energy use, bricks and mortar, and resource availability.

But the AI revolution is running up against the physical realities of electric power, water, rare earths, and electricity grids. There is an exploding demand for energy, driven by AI, the cloud, and the digital economy, as reported in Arthur D. Little’s (ADL’s) recent Blue Shift report “AI’s Hidden Dependencies.” Simultaneously, the energy transition is accelerating the growth of intermittent renewable energies, increasing the pressure on energy grids.

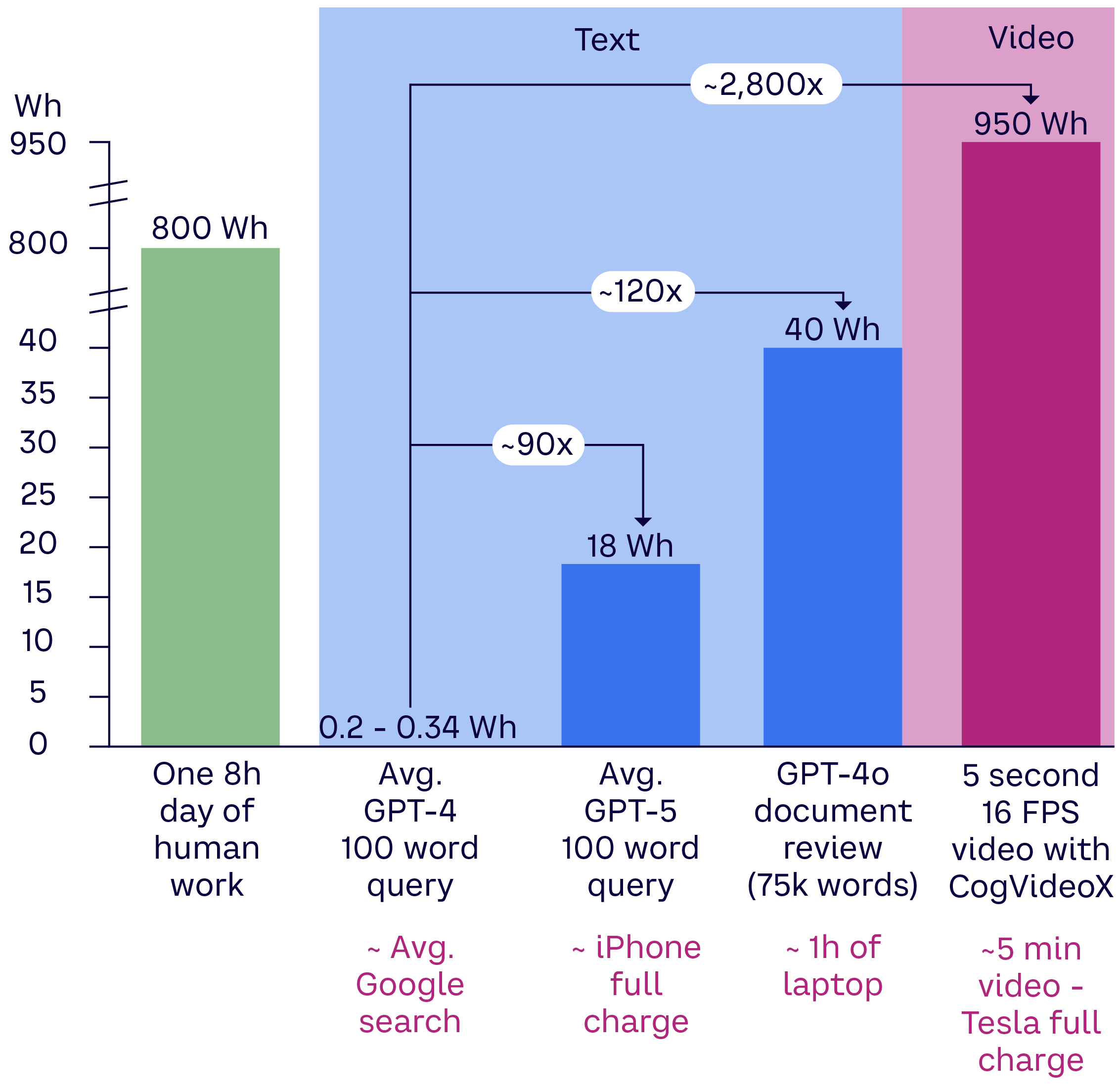

AI’s energy demand will increase exponentially as tasks increase in complexity

Source: Arthur D. Little, EpochAI, MIT Technology Review, expert interviews

When Mega-Trends Collide

“AI is changing how the economy will be driven and the way we work — and the energy requirement is huge,” says Luis del Barrio, Partner in ADL’s Energy, Utilities & Resources practice.

These mega-trends are colliding, del Barrio explains. The energy transition has been driving a move toward a decentralized power system that, in many countries, is dominated by intermittent renewable energy sources and, ultimately, storage that prizes flexibility over always-on baseload power. But the digital economy, and AI in particular, has a seemingly insatiable appetite for reliable 24/7 power — and little flexibility to change that. “Reliability will be king in the new AI world,” says del Barrio.

This is not just an issue for data center operators. Problems at these facilities can cascade across the global economy, as the AWS outage in October 2025 showed. The failure, at a hub in Northern Virginia in the US, disrupted 10,000-30,000 websites, affecting government systems, financial apps, and social media platforms worldwide.

As the computational intensity of AI training and inference (putting that training to work to perform real-world tasks) surges, energy consumption and resource use by data centers could grow fivefold, and their emissions could double by 2030, according to the previously mentioned ADL Blue Shift report. “Every AI model rests on a substantial industrial backbone of rare earths, manufacturing, electricity, and water,” the report notes. Dependence on these resources makes the sector vulnerable to issues that could affect future growth, including the availability of energy and compute infrastructure and environmental impacts.

Global data center capacity is about 50-60 GW on average and predicted to reach about 130 GW by 2028, with investment in data centers approaching US $1 trillion by 2030. According to the International Energy Agency (IEA), the sector’s electricity use is expected to double to 3% of total demand by 2030.

A key challenge for AI is that — just as the sector as a whole is scaling up extremely quickly — individual data centers are also expanding. Facilities built pre-2020 averaged tens of megawatts; today’s facilities can be 100 MW. Several 300-500 MW facilities are being built, and a number of gigawatt-scale data center campuses are under construction. (For more on the influx of global giga-scale data centers, see ADL Viewpoint “Giga Scale: The AI Infrastructure Gold Rush.”)

CONTRIBUTORS

Luis del Barrio Castro

Partner, Energy, Utilities & Resources

Michael Kruse

Managing Partner, Energy, Utilities & Resources

Sean McDevitt

Partner, Telecommunication, IT, Media & Electronics

Lars Riegel

Partner, Telecommunication, IT, Media & Electronics

Michael Liebreich

Energy Analyst & Founder, Bloomberg New Energy Finance

Dr. Albert Meige

Global Director, Blue Shift and Lead Author, AI's Hidden Dependencies

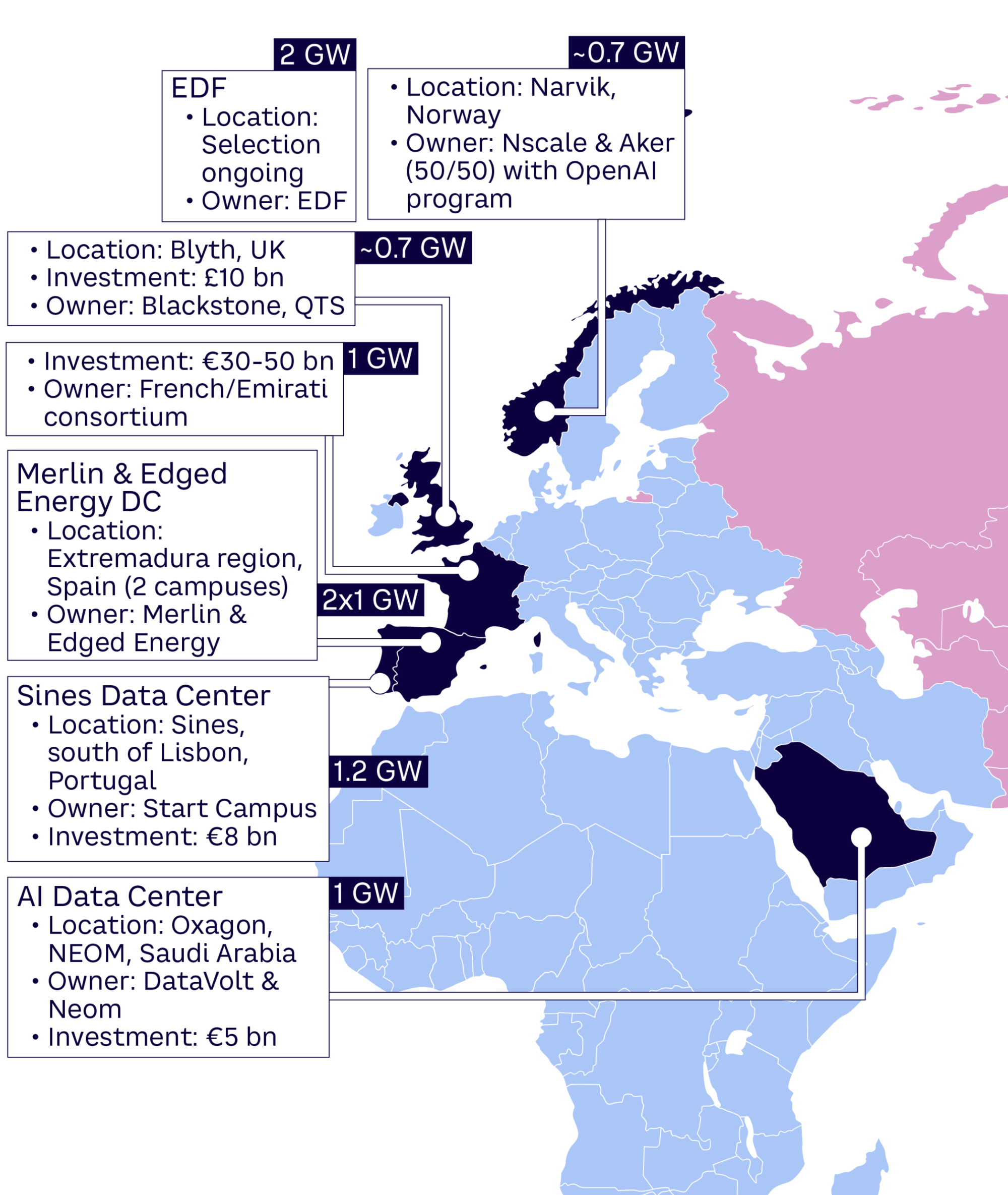

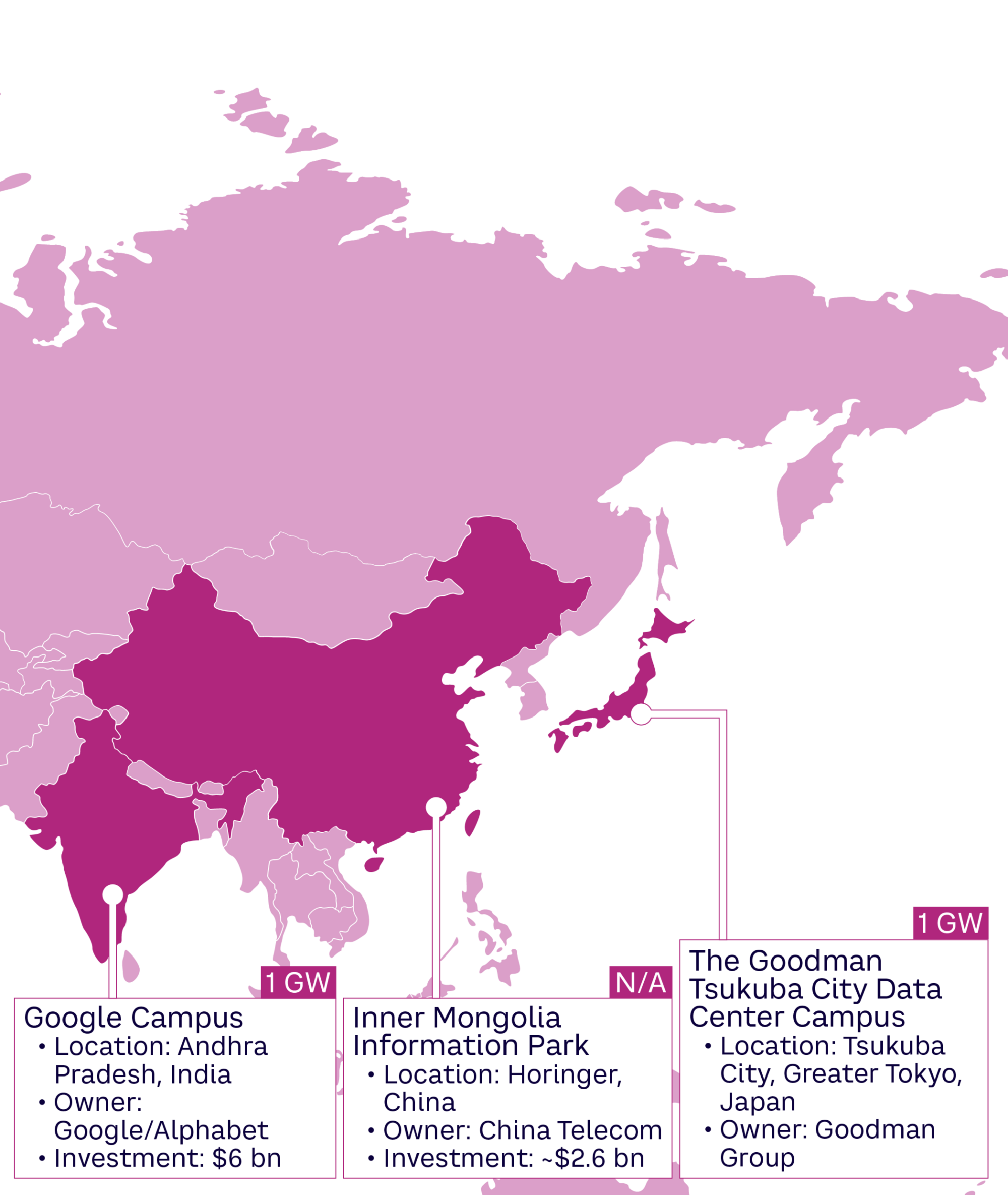

Giga-scale data center announcements

Source: Arthur D. Little, DCD, Morningstar, press releases, company announcements, Semafor, Reuters

This massively increases the amount of energy, land, and water they need. Some large data centers can draw down as much water each day as a medium-sized town, and operators are increasingly having to install closed-loop liquid-cooling systems, adding to the cost and complexity of their facilities (see ADL Viewpoint “Unlocking Cross-Industry Value: Strategic Ways to Enhance Data Center Power Needs”).

Because facilities are concentrated in certain areas, that 3% of global electricity demand is unevenly distributed. Northern Virginia hosts more than a third of global hyperscale data centers, and some studies suggest these facilities could account for 30%-45% of the state’s electricity demand by 2030. In Ireland, more than a fifth of the country’s electricity powers data centers.

Thirst For Power

AI and digital power demands are running up against demands from other industries and societal requirements. This will affect the industry’s ability to continue growing without restraint and may affect its social license to operate. “In Dublin, one of the main data center locations in Europe, energy consumption from the sector is so high that there is a moratorium on developments for the foreseeable future,” says Lars Riegel, Partner with ADL’s Telecommunication, IT, Media & Electronics (TIME) practice.

The Financial Times reports that “US data centres developers are flooding utilities with inflated growth plans, muddying efforts to plan for future power needs with projects that may never materialise. Developers are approaching multiple utilities with the same project in a quest to find the lowest-priced power, leading to so-called phantom data centres.”

In response, utilities are tightening rules and changing pricing structures to ensure that other customers do not end up paying for data center infrastructure development. This has led to data centers becoming increasingly dispersed, with hubs springing up in Milan, Madrid, the Nordics, and Eastern Europe.

Michael Liebreich, energy analyst and founder of Bloomberg New Energy Finance, says hyperscalers have suffered a rude awakening. “Suddenly these masters of the universe said, ‘Wait a minute, well, there isn’t enough electricity,’ and they were most annoyed because something as prosaic as electricity was going to get between them and their intergalactic ambitions.”

AI companies are having to integrate resource efficiency into their thinking, so the locus of innovation will switch to efficiency, Liebreich explains. They are also on the hunt for new sources of low-carbon baseload power, although they are sourcing fossil fuel energy as well, increasing emissions just as many other parts of the economy are decarbonizing. Such is the sector’s thirst for power that it has contributed to a global shortage of gas turbines, which is slowing the addition of the generating capacity it craves.

Is Nuclear The Answer?

The AI sector is one of the main drivers of a renewed appetite for nuclear power. This stems from (1) its ability to provide power that is low-carbon and consistent and (2) favorable lifecycle costs for plants and grids. Companies, including Microsoft and Meta, have sought to restart shuttered nuclear power plants or extend the life of existing facilities. Companies like Alphabet and Amazon seem more interested in small modular reactors (SMRs). These have an output of 300 MW or less and are, in theory, faster to build (they can be assembled in factories off-site), less expensive, and safer than utility-scale plants (see ADL report “The Growth & Future of Small Modular Reactors”).

Traditional engineering companies such as GE/Hitachi and Rolls-Royce, as well as China’s CNNC (China National Nuclear Corporation), are working on plants that are fairly close in concept to today’s large-scale light-water reactors. The first commercial light-water SMRs are expected to come online around 2030. China is commissioning a pre-commercial plant (the ACP100) that is due to come online in 2026.

“But the large tech companies are working with companies such as Kairos and X-energy, which are trialing different designs that (if everything works out) have a number of advantages over light-water designs,” says Michael Kruse, Managing Partner for ADL’s Energy, Utilities & Resources practice.

The coolants used in these reactors need less water, making it easier to get approval to build plants in water-stressed areas. They also use innovative fuels that produce much less waste, making it easier and less expensive to manage and dispose of. They have advanced safety features that require a smaller emergency planning zone, so reactors can be built closer to where they are needed.

“This makes it easier to colocate data centers and SMRs and to build facilities with a smaller footprint,” says Kruse. “If the industry relies only on electricity networks and renewables, the rollout of AI will be delayed because there will be competition for energy from electric vehicle charging, industrial electrification, and other sources.”

Nuclear Challenges

However, there are more than 90 innovative reactor designs being explored, says Kruse. “There is no global harmonization on designs, licensing, or supply chains. There will need to be a shakeout: the world can only sustain five or 10 dominant SMR designs because we need mass production to bring down costs. But where nuclear power was previously driven by government interests, it is now being driven by tech companies.”

The sector has a history of escalating costs and overruns, he notes. “And if you build hundreds of data centers and SMRs in remote, isolated locations or emerging countries, you are going to run into significant issues around both nuclear safety and physical/cyber security.”

Liebreich sounds a further note of caution as to why nuclear may not be the answer to the sector’s problems: “They’re going to find it’s complicated. It’s slow. When one of those reactors goes down, all of them have to be pulled offline to check the cracks or whatever it is. They’re going to find it very hard.”

There are serious constraints to growth around grid networks, too, which are aging and experiencing increased congestion due to renewables. Experts point out that although AI may appear global, its expansion depends heavily on local grid capacity and connection speed. In parts of the US and Europe, projects are waiting up to seven years to get connected, delaying projects despite available capital.

More Transparency Needed

AI and data centers have grown so quickly that it is increasingly difficult to know how much energy the sector is using. “Since 2024, fewer than 3% of new AI models have disclosed environmental data, down from 10% in 2023,” says Sean McDevitt, Partner in ADL’s TIME practice. Voluntary disclosure regimes are inadequate, and they fail to create a baseline from which the industry (as well as regulators, policymakers, and investors) can measure improvements in energy intensity.

The above-mentioned Blue Shift report notes: “What we know about AI’s footprint is a function of what’s chosen to be reported and is incomplete. Even where reporting exists, data is partial, incomparable, or framed to understate impact. Without consistent, mandatory disclosure, its real footprint will remain unknown.”

Regulations vary widely from region to region. China has set national targets for data center efficiency and renewable energy use, and under the EU’s Energy Efficiency Directive, data centers over 500 kW must disclose their energy and water use, as well as how efficient they are. In the US, there is no federal mandate, so rules differ from state to state.

It is even harder to discern how much energy AI is saving across the rest of the economy. But with the energy crunch intensifying, the sector will have to quantify its energy usage and explain how it helps other sectors save energy if it wants to maintain its social license to operate.

Energy-saving Innovations

“Innovations are starting to emerge to limit AI’s energy consumption and disruptive impact on other sectors,” says Riegel. Chips are becoming more efficient, and creating specialized models for specific tasks makes them more effective. AI training that is not time- and location-sensitive is quite portable. It can be moved to times of low demand or grids with high levels of renewable energy, either permanently by siting data centers in remote locations with a lot of land and low-carbon power, or temporarily, to reduce pressure on networks at peak time and leverage lower power prices or the availability of renewables (see ADL Viewpoint “Hybrid Renewable Ecosystems”). Much of the work can be done directly on devices such as phones or laptops, reducing reliance on data centers.

Given that the geographical concentration of data centers causes strains on specific electricity grids, nonprofit Rewiring America has suggested that hyperscalers looking for quick access to power could pay householders to install heat pumps in regions where they want to build data centers, freeing up the electricity they need. In the US state of Pennsylvania, the group says, data centers will add about 3 GW of new demand to the grid, but 45% of that demand (about 1.3 GW) could be offset just by replacing inefficient electric heating with heat pumps. If hyperscalers subsidized half the cost of heat pumps for households, they could free up capacity at a similar cost to building and operating a new gas-fired power plant while generating consumer goodwill and helping decarbonize the housing stock, the group notes.

Next Steps

The energy crunch is coming, and AI is both a cause and a victim. Companies in the sector can take several “no-regret” actions to ensure they are prepared for the new risks this will create. These include an increased focus on resource efficiency, as well as working to create credible environmental reporting of AI’s impacts. They should also engage with transmission system operators (TSOs), not just to gain access to the grid, but to propose innovative ways to free up capacity.

The sector’s growth has been characterized by a “throw money at the problem” approach. As it comes up against the physical limitations of power availability, the sector’s ability to thrive will depend on how quickly it can pivot to more innovative, sustainable solutions.

Key Takeaways

- AI’s demand for energy is coming up against real-world physical constraints that could limit growth. Both providers and end users should consider how they can reduce these constraints to reduce their exposure to shocks.

- Grid capacity is as important as power availability. Data center providers should engage with TSOs to understand how facilities can fit into grid networks.

- More transparency is needed around AI’s energy and resource use. End users are likely to begin demanding this information as part of their AI procurement process.

- Nuclear power, especially SMRs, may help to ease AI’s energy crunch, but it may take longer than expected to make an impact.

- There are quick wins available by cutting energy demand through the development of more efficient chips and algorithms, as well as by moving AI training to areas and times where power demand is lower or supply is low-carbon.

- Providers should map their supply chains and diversify their exposure to increase resilience in the face of potential geopolitical and operational disruptions.

This article builds directly on AI’s Hidden Dependencies and draws extensively on its framing, analysis, data and visuals. We thank the Blue Shift team for the work that underpins this piece.